Complete Guide to Payroll Tax Registration for New Employers

Payroll tax registration is the mandatory process by which employers establish official accounts with federal and state tax authorities to withhold and remit employment taxes, enabling legal payroll processing and employee hiring. Once you begin paying employees, registration is generally required before or shortly after you pay your first wages, depending on each state’s thresholds.

This guide explains the complete registration process for federal and state payroll tax accounts, including required documentation, step‑by‑step procedures, and timeline expectations. It is designed for new employers, business owners launching their first venture, and companies expanding into additional states. Understanding these requirements matters because failure to register properly can result in penalties, delayed payrolls, and loss of valuable federal tax credits.

Direct answer: You must have payroll tax registrations in place before your first payroll date or within the time frame specified by each state—this includes a federal Employer Identification Number (EIN) and the appropriate state income tax withholding (if applicable) and unemployment insurance accounts in every state where you employ people.

By reading this guide, you will:

- Understand federal and state payroll tax registration requirements.

- Follow a practical step‑by‑step process for completing all registrations.

- Gather the correct documentation before registration begins.

- Set realistic timeline expectations for processing.

- Maintain compliance and avoid common registration pitfalls.

Key Takeaways

- You cannot run compliant payroll or claim key tax credits until your federal and state payroll tax registrations are in place.

- Every state where employees work—not just your home state—can require its own withholding and unemployment accounts.

- States without wage‑based income tax (like Texas and Florida) still require unemployment registration and often electronic tax payments.

- Registration timelines vary widely, from instant online approvals to several weeks, so starting 2–4 weeks before first payroll is a practical minimum.

- Payroll providers typically rely on you to supply EINs and state account numbers; they usually do not open tax accounts, which is where specialized services like LicenseComply step in.

Understanding Payroll Tax Registration

Payroll tax registration establishes the official accounts your business needs to withhold taxes from employee wages and pay employer‑portion taxes to government agencies. Without these registrations, you generally cannot legally pay employees, file required payroll tax returns, or deposit payroll taxes.

When you start hiring employees, registration becomes mandatory once you meet federal and state thresholds. Employees earn taxable wages, and you as the employer must withhold income tax, Social Security, and Medicare from their pay while also contributing unemployment taxes at the federal and state levels.

Federal Payroll Tax Registration

Federal payroll tax registration centers on obtaining an Employer Identification Number (EIN) from the IRS—also called a taxpayer ID number or federal employer identification number. This nine‑digit number identifies your business to the federal government for all tax purposes, including payroll, income, and information returns.

Your federal payroll tax obligations include:

- Withholding federal income tax from employee wages.

- Withholding and matching Social Security and Medicare taxes (FICA).

- Paying Federal Unemployment Tax Act (FUTA) taxes, generally calculated at 6% on the first 7,000 of each employee’s wages, with a credit of up to 5.4% for timely state unemployment contributions, effectively reducing the rate to 0.6% for most compliant employers.

Because the EIN underpins your entire tax profile, most state payroll registrations and payroll service setups depend on it.

State Payroll Tax Registration

State payroll tax registration varies significantly by jurisdiction. Most states require two primary employer registrations:

- A withholding account for state income tax withheld from employee pay.

- An unemployment insurance (UI/SUTA) account for employer unemployment contributions and quarterly wage reporting.

States such as Texas, Florida, Nevada, South Dakota, Tennessee, Washington, Wyoming, Alaska, and New Hampshire do not impose a traditional wage‑based state income tax, so employers there typically register only for unemployment insurance and any applicable local payroll‑type taxes. Other states combine registrations or require additional accounts for disability insurance or paid family leave programs.

In nearly every jurisdiction, you will need your existing EIN to apply for state payroll tax accounts.

Registration Requirements and Documentation

Before any applications are submitted, it is important to assemble the information and supporting documentation that federal and state agencies will request.

Essential Business Information

Agencies typically require:

- Complete legal business name exactly as shown on formation documents.

- Business structure (corporation, limited liability company, partnership, or sole proprietorship).

- Principal business address, mailing address, and any additional operating locations.

- Names, titles, and identifying information for owners, officers, or responsible parties.

You will also need details about payroll plans, including expected first pay date, pay frequency, anticipated number of employees, and projected quarterly wages. These factors influence filing schedules, deposit frequencies, and sometimes new‑employer unemployment tax rates.

Required Documentation

Commonly requested documents include:

- Articles of incorporation, articles of organization, or partnership agreements.

- EIN confirmation notice (such as IRS CP 575).

- Business licenses and permits for your operating jurisdiction.

- Foreign qualification documents for states where you operate beyond your formation state.

- Registered agent details in each state where you are registered to do business.

Having these organized in advance helps ensure smoother, faster registrations.

Timeline Considerations

Planning ahead is critical because processing times differ across agencies and seasons.

Starting 2–4 weeks before your first planned payroll is a practical baseline for most employers. While the EIN can be issued almost immediately when requested electronically, state processing times range from near‑instant online approvals to 3–10 business days, and some jurisdictions can stretch to several weeks during busy periods.

In California, for example, you must register with the Employment Development Department (EDD) once you pay more than 100 in wages in a calendar quarter to one or more employees, and employers are expected to complete registration shortly after crossing that threshold. Many other states require registration before or very soon after your first payroll, making early planning essential.

Payroll processors generally cannot run payroll or file and deposit taxes until they receive your EIN and the applicable state account numbers, such as withholding and unemployment insurance accounts.

Step‑by‑Step Payroll Tax Registration Process

Registration Procedure (High‑Level)

- Confirm entity setup and EIN

Ensure your business entity is properly formed and has a valid EIN that can be used for federal and state payroll registrations. The EIN is the anchor ID for your employer payroll obligations at the federal level and is required by most states. - Confirm state authority to do business

For each state where you have or will have employees, confirm that the entity is registered to transact business (including foreign qualification where required) and that a registered agent is in place. Many state tax and workforce agencies check entity status before issuing employer accounts. - Set up or request state withholding accounts (if applicable)

In states that impose a wage‑based income tax, an employer withholding account is required so you can remit employees’ withheld state income taxes. These registrations are typically completed with the state department of revenue or taxation using online portals such as myconneCT (Connecticut), MyTax Illinois, or Georgia Tax Center. - Register for state unemployment insurance (SUTA/UI)

State unemployment accounts are opened with the state’s labor, workforce development, or employment security agency and are used to file quarterly wage reports and pay state unemployment contributions. Modern systems like Indiana’s Uplink Employer Self Service and similar portals often issue account numbers quickly once applications are complete. - Determine deposit and filing schedules

Agencies assign deposit and filing frequencies based on projected or actual tax liability. These schedules govern how often payroll taxes must be remitted and when returns are due, so they must be captured accurately and shared with whoever runs payroll. - Integrate account details into payroll systems

Once federal and state IDs are in place, they are provided to payroll platforms or internal payroll teams so that withholdings, deposits, and filings are made under the correct accounts. Maintaining a consolidated list of IDs and access credentials is essential for ongoing compliance. - Establish payroll tax record‑keeping

Employers must maintain detailed payroll records, including gross wages, taxable wages, pre‑tax deductions, tax withholdings, and net pay for each employee. These records support quarterly and annual payroll filings and are often requested during audits or agency inquiries.

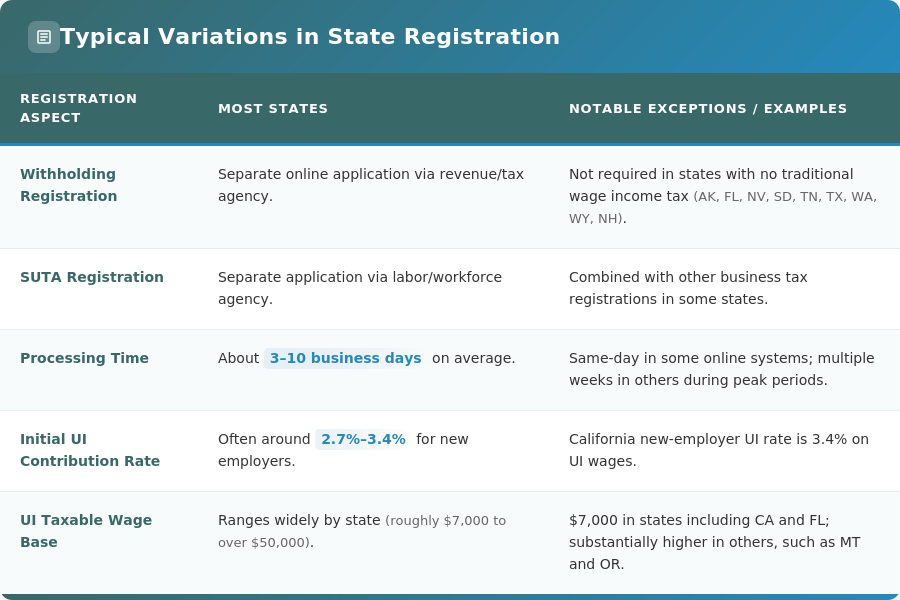

State‑by‑State Variations

Each state sets its own rules for registration, rates, and wage bases, which can significantly affect cost and complexity.

Typical Variations

For multi‑state employers, this means each expansion into a new state can trigger separate registrations, different wage bases, and distinct reporting schedules.

Common Registration Challenges and Solutions

New employers often encounter the same issues when navigating payroll tax registration; awareness helps you plan around them.

Missing or Incomplete Documentation

Applications are frequently delayed because formation documents, EIN confirmation, officer data, or address details are missing or inconsistent. Using a standardized checklist for each state and verifying that all information is consistent across agencies reduces rejections and processing delays.

Delayed Processing Times

High‑volume periods (such as year‑end or major law changes) can extend processing times beyond posted estimates. Monitoring application status via online portals and allowing enough lead time before your first payroll reduces the risk of needing to postpone pay dates or issue manual checks without proper accounts.

Multi‑State Registration Complexity

Companies with employees in several states must track different thresholds, forms, portals, deadlines, and wage bases simultaneously. For organizations operating in five or more states, it is common to engage specialized payroll tax registration services that handle state‑by‑state applications, coordinate with agencies, and centralize approvals and account credentials.

Role of Payroll Providers

National payroll services calculate taxes, generate paychecks, and file ongoing payroll returns once accounts are set up, but they typically do not open tax accounts with government agencies. That means employer registrations still need to be completed separately, often with the support of third‑party registration specialists.

Conclusion and Next Steps

Completing payroll tax registration before your first payroll protects your business from penalties, ensures employees have the correct taxes withheld from day one, and preserves your eligibility for FUTA credits worth up to 5.4% of taxable wages. Proper registration lays the foundation for every payroll you run in the future, from your first hire to multi‑state expansion.

After registrations are in place, employers must:

- File required employer returns and quarterly wage reports on time each quarter.

- Deposit payroll taxes according to the schedules assigned by each agency.

- Maintain accurate payroll and employee records for auditing and compliance.

- Update registrations when expanding into new states or changing business information such as addresses, ownership, or entity type.

A specialist like LicenseComply can coordinate the entire payroll tax registration process—federal and state—so that by the time you are ready to run payroll, your accounts are established, your obligations are mapped out, and your business is positioned for compliant growth.

Disclaimer: This material is provided for general informational and educational purposes only and should not be construed as legal, tax, or accounting advice. While LicenseComply strives to ensure the accuracy and timeliness of the information presented, laws, regulations, and administrative guidance are subject to change. No guarantee or warranty is made as to the completeness, accuracy, or applicability of this content to any specific situation. You should consult a qualified attorney, tax advisor, or accountant who can assess your individual circumstances before making business, compliance, or financial decisions.